All companies are at one of five stages of maturity in their sustainability practices, and they can all be helped to progress towards ‘Champion’ status

Why have companies such as Amazon, Google and Starbucks attracted such opprobrium over their corporate tax strategies?

Do global drinks companies have any responsibilities for the social, economic and environmental (SEE) impacts of the misuse of their products beyond what may be imposed by different national laws?

How do some FMCG and retail companies repeatedly find new business opportunities from voluntarily accepting higher standards of SEE performance while others find it necessary to compromise suppliers’ interests in order to survive?

What makes a handful of businesses share technologies and intellectual property and form collaborations with NGOs (and even competitors) to further sustainable development ?

We assert that the answer to these questions depends on the “corporate responsibility stage of maturity” that a company has reached, the responsibility a business takes for its SEE impacts and the purpose of business. Several writers have set out various descriptions of such stages .

This approach is by no means academic. Responsible 100 is an organisation that helps companies to respond to stakeholder concerns and promotes greater transparency and accountability by evaluating companies actions to be at one of four stages: unacceptable, justifiable, commendable and exemplary. The Dutch financial group Rabobank assesses its customers’ responsible business practices against four stages: inactive, reactive, active and proactive. The common goal of these models is to help companies to understand where they are, and to develop a road map for improvement.

In our model we set out five stages on a path to corporate sustainability which we define as “a business commitment to sustainable development and an approach that creates long-term shareholder and societal value by embracing the opportunities and managing the risks associated with social, environmental and economic developments” . We suggest corporate sustainability is a higher stage than corporate responsibility.

- Deniers believe they have no responsibility for their SEE impacts beyond the law.

- Compliers simply meet minimum legal requirements and any locally prevailing business standards in each of the markets in which they are operating. For companies doing business internationally this may lead to inconsistencies in their approach in different parts of the world.

- Others take a more active approach: Risk Mitigators.

- Opportunity Maximisers move beyond finding commercially attractive opportunities on a regular, systemic basis from a commitment to sustainability.

- We envisage companies moving to a higher stage, becoming Champions, who will engage their value-chains in sustainable production and consumption, share technologies and expertise, and work in transformational partnerships with other companies and other parts of society.

We suggest that a company’s stage of maturity is based on a mixture of mindset; business purpose, strategy, organisation and policies; and results.

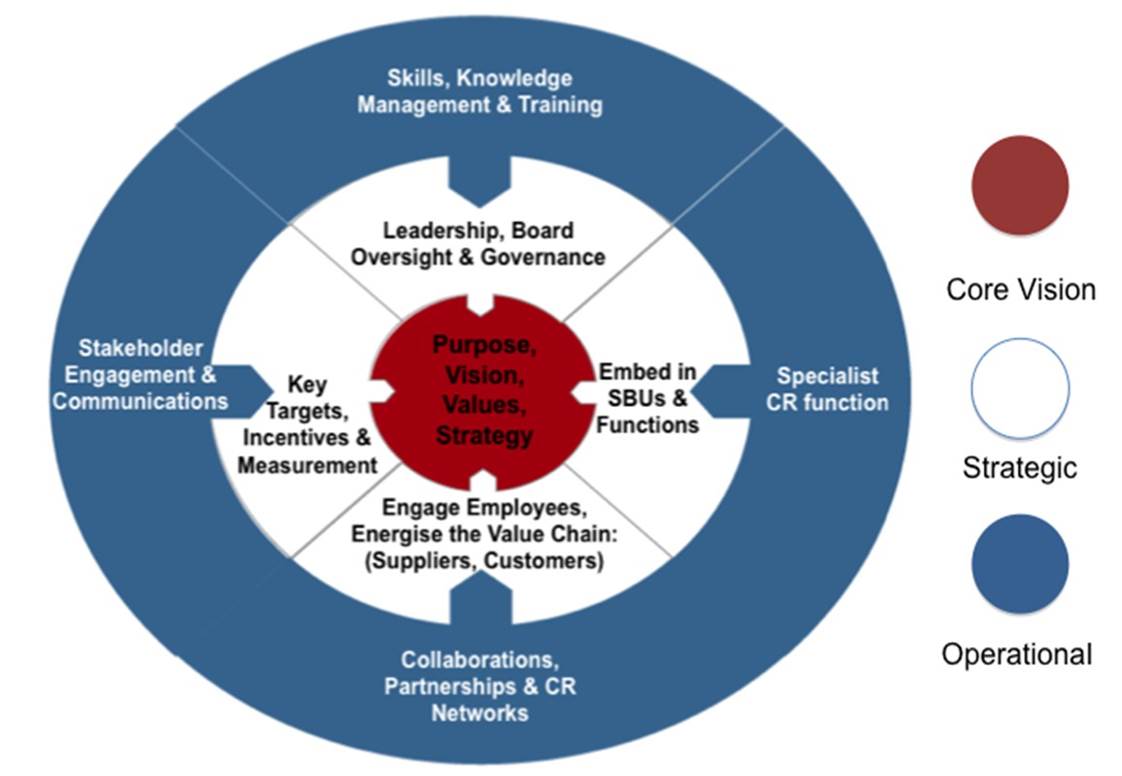

Figure 1. Embedding sustainability model

Fig. 1 shows some potential dimensions of mindset and how these will shift with stage of maturity. The major focus, however, has been on business purpose, strategy, organisation and policies. Based on a Cranfield doctoral thesis by David Ferguson, the Doughty Centre has developed a model for embedding corporate responsibility: fig 2. Clearly, how a company approaches each element of the embedding model will depend on their mindset. Thus, for example, a denier company board is unlikely to have any oversight of, or take responsibility for, the company’s SEE impacts. By contrast, an opportunity-maximiser will have a collective board mindset for corporate sustainability.

Figure 2. Evolution of stages of maturity

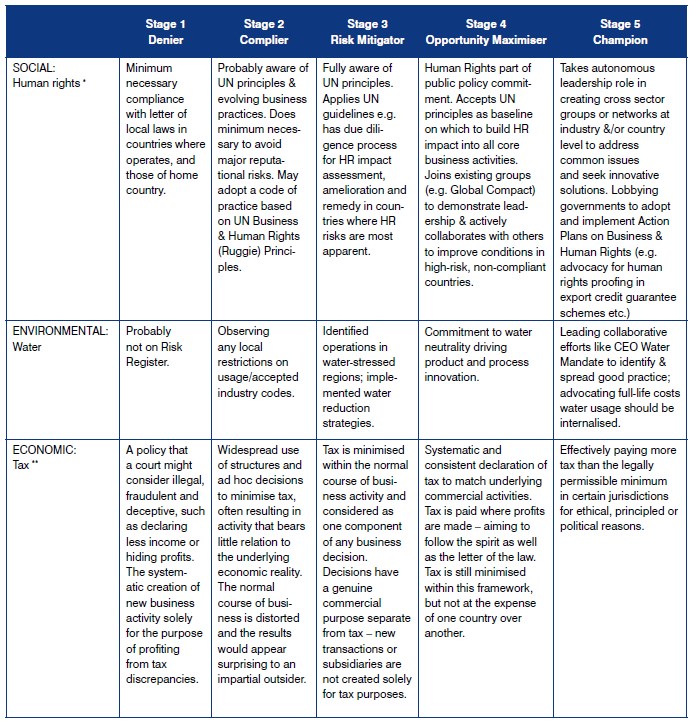

Companies will respond to SEE issues very differently at different stages of maturity as illustrated with three significant SEE issues: fig 3.

Figure 3. Managing illustrative sustainability issues at different stages of maturity

We suggest stage of maturity is not just about intent and structures but also about results. Over time, we would expect to see the opportunity maximisers demonstrating superior results both in terms of sustainability and financial performance, as recent research suggests . Accenture’s 2013 CEOs’ survey for the UN Global Compact showed that only a small proportion of the UNGC companies participating in the survey were these high-performers on both sustainability and financial performance. Such superior results might be assumed to give greater confidence and credibility to these companies to evolve in the future into Champions.

We do not see any of these stage 5 companies yet (although we see a few showing some attributes) and there are still only very few multinational companies that are truly at stage 4.

Large multinational companies may have a dominant stage of maturity but their different country operations and strategic business units may be at very different stages. Companies setting ambitious targets around responsible business practices and even committing to corporate sustainability face reputational risks from laggard operations.

Rising expectations

What we postulate is based on current good practice. However, as this concept spreads and is adopted more widely, the bar will continue to rise. Thus, 15 years ago, some form of corporate responsibility reporting might have been regarded as innovative and forward-thinking. Today, for large companies, it would be merely Compliant. Similarly, today a commitment to circular economy practices could be considered stage 4 or 5 but in a decade’s time will probably be seen as Complier stage.

We recognise that there will be variations in what is possible for a company, depending on where it is within its industry and value-chain: what being a Champion would look like for, say, a Walmart, will be different to, say, one of its third-tier suppliers.

We suggest that what is needed for a Champion company to emerge requires a company to be operating at Champion level within all the elements of our target, in all strategic business units (SBUs) in all parts of the world where it operates.

As social media and stakeholder expectations drive greater corporate transparency and accountability, there will be a premium on business leaders with the skill and will to engage and empower their organisation and their value-chain to take responsibility for driving up ethical and sustainability standards and results. This is both a challenge and an opportunity.

This is an abridged version of “Business Critical: Understanding a Company’s Current and Desired Stages of Corporate Responsibility Maturity”, published by the Doughty Centre. www.doughtycentre.info

http://www.som.cranfield.ac.uk/som/dinamic-content/media/Doughty/SOMAT%201505%202014%20final.pdf

David Grayson is director of the Cranfield University Doughty Centre for Corporate Responsibility and Ron Ainsbury is a visiting fellow of the Centre.

Essay measuring sustainability SEE sustainability agenda sustainable development